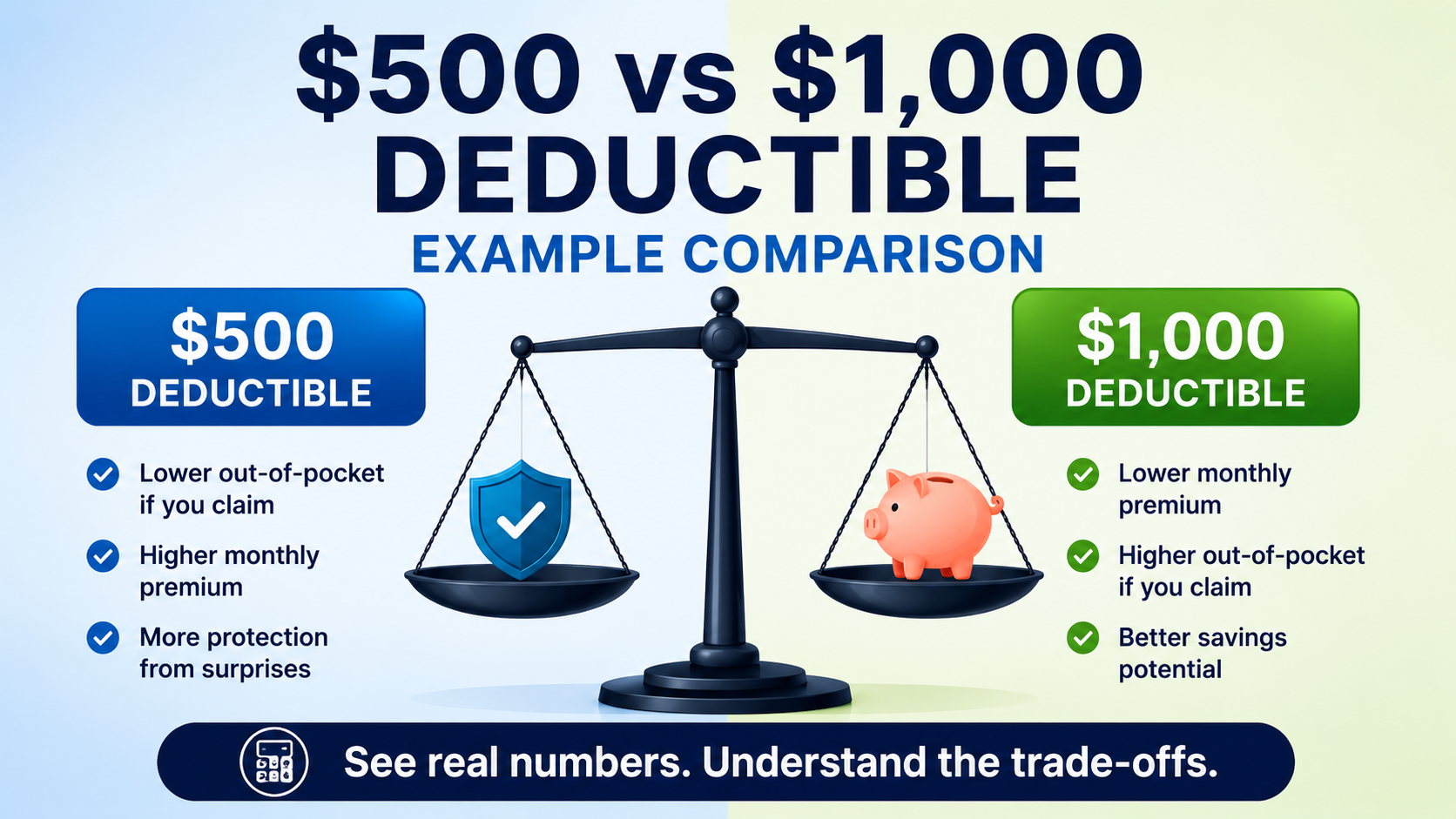

Quick answer: what changes between a $500 and $1,000 deductible?

Moving from a $500 deductible to a $1,000 deductible may lower your monthly premium, but it also adds $500 of extra out-of-pocket risk if a covered claim happens.

In this example, the higher deductible saves $18 per month, or $216 per year. That means it takes about 28 claim-free months for the premium savings to match the extra $500 deductible risk.

The higher deductible may look reasonable if you can comfortably pay the extra $500 and you are comfortable with the claim risk. It may look weaker if the savings are small or a claim happens soon.

In plain English: lower premium means taking more claim risk

A deductible is the amount you may need to pay yourself before insurance pays for a covered claim.

A premium is the amount you pay to keep the policy active. In many cases, a higher deductible can lower the premium because you are agreeing to pay more yourself if a claim happens.

That is the basic tradeoff. A $1,000 deductible may save money every month, but it also means a higher bill if you need to file a covered claim.

Simple rule: compare the monthly savings with the extra deductible amount you may need to pay if a claim happens.

Example: $500 deductible vs $1,000 deductible

Suppose you are comparing two deductible options for the same type of insurance policy:

| Item | $500 deductible option | $1,000 deductible option |

| Deductible | $500 | $1,000 |

| Monthly premium | $140 | $122 |

| Monthly savings | — | $18 |

| Annual premium cost | $1,680 | $1,464 |

| Annual savings | — | $216 |

In this example, the $1,000 deductible saves $18 per month, or $216 per year.

But it also increases the deductible from $500 to $1,000. That means you may need to pay $500 more out of pocket if a covered claim happens.

| Comparison | Amount |

| Annual premium savings | $216 |

| Extra deductible risk | $500 |

| Break-even estimate | About 28 claim-free months |

This is not automatically a good or bad tradeoff. It depends on whether the savings are worth the added claim risk.

Why claim timing matters

Premium savings build slowly. Deductible risk can appear immediately.

If no claim happens for several years, the higher deductible may save money. If a claim happens soon, the higher deductible may cost more overall.

| Claim timing | Savings collected | Extra deductible risk | Simple result |

| After 6 months | $108 | $500 | -$392 |

| After 1 year | $216 | $500 | -$284 |

| After 2 years | $432 | $500 | -$68 |

| After 30 months | $540 | $500 | +$40 |

In this example, the higher deductible only starts to look better after roughly 28 claim-free months.

The simple break-even calculation

The break-even point estimates how long the premium savings need to build before they match the extra deductible risk.

| Step | Calculation |

| Extra deductible risk | $1,000 – $500 = $500 |

| Monthly premium savings | $140 – $122 = $18 |

| Break-even estimate | $500 ÷ $18 = about 27.8 months |

What this means: the higher deductible needs about 28 claim-free months before the savings match the extra $500 you may need to pay if a claim happens.

You can read more about this idea in the guide to the deductible break-even point.

Better tradeoff vs weaker tradeoff

The $1,000 deductible looks better when the savings are large enough and the extra deductible risk is manageable. It looks weaker when the premium savings are small or the claim risk feels too high.

| Scenario | Monthly savings | Extra deductible risk | Break-even estimate | Comment |

| Weak tradeoff | $8 | $500 | About 62.5 months | Savings are small compared with the added risk |

| Moderate tradeoff | $18 | $500 | About 28 months | Worth reviewing carefully |

| Stronger tradeoff | $45 | $500 | About 11 months | Savings catch up faster |

A shorter break-even period usually means the savings catch up faster. A longer break-even period means you carry the added claim risk for longer before the savings may make up for it.

Common mistake: looking only at the monthly premium

The most common mistake is treating the lower premium as the full story.

Saving $18 per month can feel attractive. But if one covered claim happens before enough savings build up, the higher deductible may cost more overall.

Simple warning: a lower premium is not the same as lower total risk. It is a tradeoff between regular savings and possible claim cost.

What to check before choosing between $500 and $1,000

- How much would the monthly premium actually decrease?

- How much would you save per year?

- How much extra deductible risk would you take?

- How many claim-free months are needed to break even?

- Could you comfortably pay the $1,000 deductible if a claim happened tomorrow?

- Would paying the higher deductible create debt or delay repairs?

- Does the deductible apply the same way to every claim type?

- Are you comparing real quotes, not rough guesses?

These checks help you compare the full deductible tradeoff, not only the monthly price difference.

When the $1,000 deductible may make sense

The $1,000 deductible may be reasonable when the premium savings are meaningful, the extra $500 risk is manageable, and you have enough emergency savings to handle a claim.

It may also make more sense when you are comfortable with a longer break-even period and understand that a claim can change the result quickly.

The point is not that the $1,000 deductible is better. The point is that the higher deductible needs to be compared against the full out-of-pocket risk.

For a broader comparison, see high deductible vs low deductible and premium savings vs out-of-pocket risk.

Compare your own deductible numbers

Use the DeductibleWise calculator to compare premium savings, extra deductible risk, break-even years, and one-year claim impact before changing a deductible.

$500 vs $1,000 deductible FAQ

Is a $1,000 deductible always better than a $500 deductible?

No. A $1,000 deductible may lower the premium, but it also increases the amount you may need to pay if a covered claim happens. The better fit depends on the savings, claim risk, and your ability to pay the higher deductible.

How much extra risk does a $1,000 deductible add?

Compared with a $500 deductible, a $1,000 deductible adds $500 of extra out-of-pocket risk if a covered claim happens.

How do I know if the premium savings are enough?

One simple way is to divide the extra deductible risk by the monthly premium savings. In this example, $500 divided by $18 gives a break-even estimate of about 28 months.

What is the biggest warning sign?

The biggest warning sign is a small premium saving with a large deductible increase. That usually creates a long break-even period.

Does this replace advice from an insurance professional?

No. This is an educational comparison. It does not review your full policy, coverage limits, exclusions, claim history, or personal financial situation.

Related posts

Browse all posts on the DeductibleWise Blog or see a sample DeductibleWise report.

Educational disclaimer: This content is for educational use only. It is not insurance, financial, legal, or tax advice. It does not review your full policy, coverage limits, exclusions, claim history, or personal financial situation. Review your policy terms and speak with your insurer or a qualified professional before changing coverage.