What is an insurance deductible?

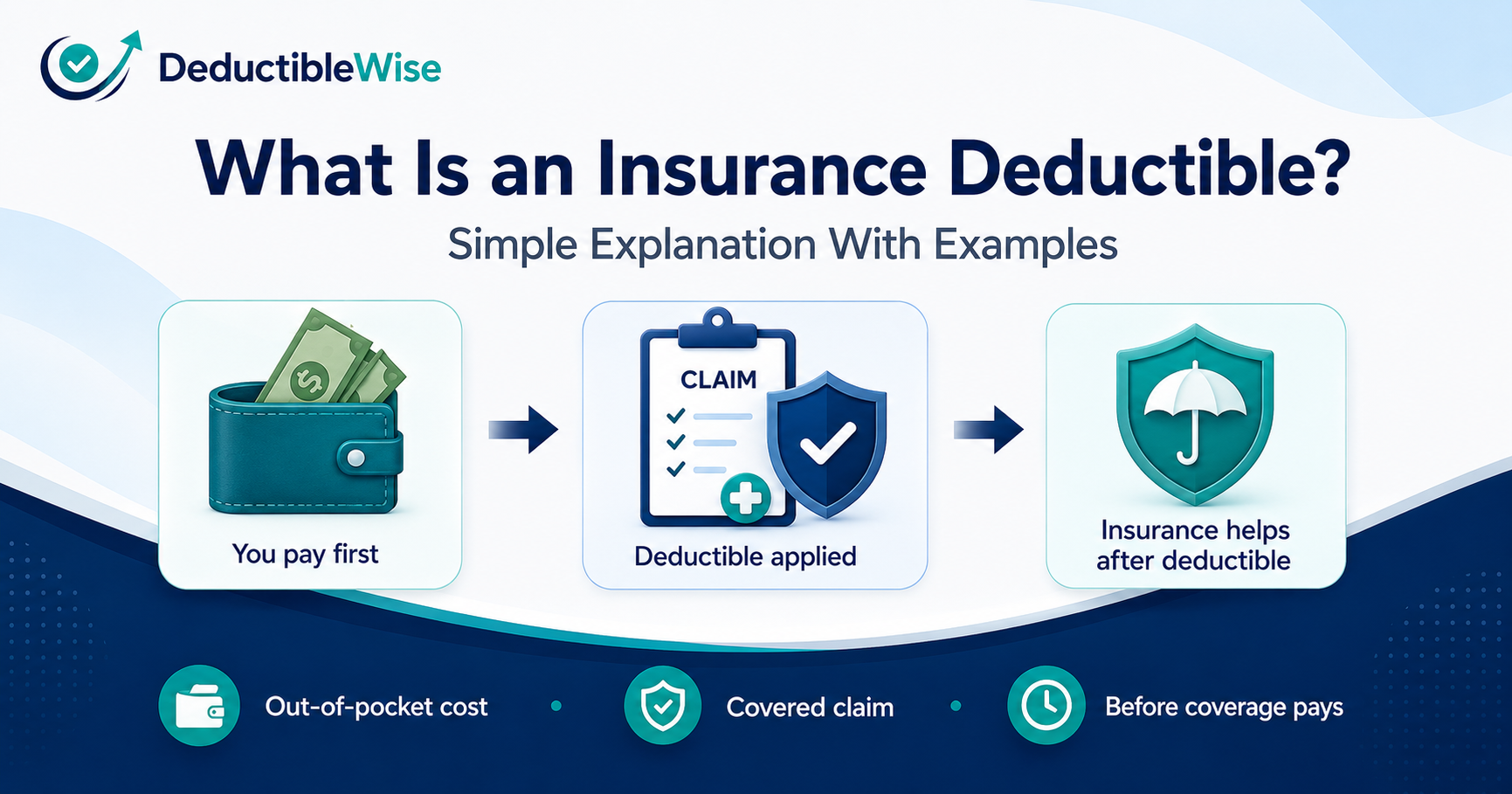

An insurance deductible is the part of a covered claim that you may need to pay yourself before the insurance company pays its share.

For example, if you have a $500 deductible and a covered claim costs $3,000, you may pay the first $500, and the insurer may pay the remaining covered amount, depending on your policy terms.

The deductible is one of the main tradeoffs in an insurance policy. A lower deductible usually means less out-of-pocket cost if a claim happens, but it may come with a higher premium. A higher deductible may lower the premium, but it can increase your cost if a claim happens.

Deductible in plain English

Think of a deductible as your first share of the bill when a covered claim happens.

If the claim is covered by your policy, the deductible is the amount you may need to pay before the insurance payment applies. The exact rules can vary by insurance type, policy, coverage section, and claim situation.

Simple way to remember it: the deductible is the amount you may need to handle before insurance starts covering the rest of a covered claim.

This is why deductible decisions are not only about saving money on premiums. They are also about how much out-of-pocket risk you are comfortable taking.

Simple deductible example

Suppose you have a car insurance policy with a $500 deductible. A covered accident creates $3,000 of repair costs.

| Item | Amount |

| Total covered repair cost | $3,000 |

| Your deductible | $500 |

| Remaining covered amount | $2,500 |

In this simple example, you may pay $500, and the insurer may cover the remaining $2,500, assuming the claim is covered and there are no other policy limits or exclusions that change the result.

This example is simplified. Real claims can depend on coverage limits, exclusions, depreciation, repair rules, fault rules, and other policy details.

Lower deductible vs higher deductible

The deductible amount affects the balance between premium cost and out-of-pocket risk.

Lower deductible

A lower deductible may reduce what you pay if a covered claim happens.

But it may also mean a higher premium.

Higher deductible

A higher deductible may reduce your premium.

But it can increase what you need to pay yourself if a claim happens.

The key question is not only “Which deductible is cheaper?” A better question is: “Are the premium savings enough to justify the extra out-of-pocket risk?”

You can read a deeper comparison here: High Deductible vs Low Deductible.

How a deductible can affect your premium

A premium is the amount you pay to keep the insurance policy active. Depending on the policy and insurer, choosing a higher deductible may reduce the premium because you are accepting more of the claim cost yourself.

But the monthly saving can look better than it really is if you do not compare it against the extra deductible risk.

| Option | Deductible | Monthly premium | Annual premium |

| Lower deductible option | $500 | $120 | $1,440 |

| Higher deductible option | $1,000 | $100 | $1,200 |

In this example, the higher deductible saves $20 per month, or $240 per year. But it also adds $500 of extra deductible risk if a covered claim happens.

That is why deductible comparisons should look at both sides of the decision: savings and risk.

Where break-even fits into the deductible decision

The break-even point estimates how many claim-free years are needed for premium savings to cover the extra deductible risk.

Using the example above:

- Extra deductible risk: $500

- Annual premium savings: $240

- Break-even estimate: about 2.1 claim-free years

This means the higher deductible needs about 2.1 claim-free years before the premium savings match the extra $500 risk.

For a fuller explanation, read: What Is a Deductible Break-Even Point?

Common mistake: choosing by premium only

A common mistake is focusing only on the lower monthly premium and ignoring the larger deductible.

Saving $20 per month may feel useful. But if the deductible increases by $500, one claim can erase more than two years of savings in this example.

That does not mean the higher deductible is wrong. It means the decision needs context: claim likelihood, cash buffer, premium savings, and personal comfort with risk.

What to check before choosing a deductible

- How much would the higher deductible save per month and per year?

- How much extra would you need to pay if a claim happens?

- Could you comfortably pay the higher deductible from savings?

- Does the deductible apply per claim or per policy period?

- Are there different deductibles for different coverage types?

- Are there exclusions or policy rules that change how the deductible applies?

- How likely is a claim based on your recent experience and situation?

These checks help turn a deductible from a vague policy number into a clearer risk decision.

Compare your own deductible options

Use the DeductibleWise calculator to compare premium savings, extra deductible risk, break-even years, and one-year claim impact using your own numbers.

Insurance deductible FAQ

Do you always pay the deductible?

Not always. It depends on the policy, the type of claim, the coverage involved, and whether the claim is covered. Some situations may have different deductible rules.

Is a lower deductible always better?

No. A lower deductible may reduce out-of-pocket cost if a claim happens, but it may also increase the premium. The better comparison is the tradeoff between premium cost and claim risk.

Is a higher deductible always riskier?

A higher deductible usually increases the amount you may need to pay if a claim happens. Whether that risk is acceptable depends on your savings, claim likelihood, and premium savings.

Can the deductible be different for different insurance types?

Yes. Auto, home, renters, health, and other insurance types can use deductibles differently. Some policies may even have different deductibles for different kinds of claims.

Related deductible guides

Educational disclaimer: This content is for educational use only. It is not insurance, financial, legal, or tax advice. It does not review your full policy, coverage limits, exclusions, claim history, or personal financial situation. Review your policy terms and speak with your insurer or a qualified professional before changing coverage.